Simple Facts About Complicated Card Brand Fees

Card brand fees appear on every merchant's processing statement — but most business owners don't know what they are. Learn what's normal, what's a penalty, and how to find them on your statement.

If you've ever looked at your monthly credit card processing statement and felt confused by the long list of fees — you're not alone. Most merchants see dozens of line items and have no idea what half of them are or where they come from.

One of the most commonly misunderstood categories is card brand fees. These are charges that come directly from the card networks — Visa, Mastercard, Discover, and American Express — and they show up on virtually every processing statement, every single month.

This guide breaks it all down: what card brand fees are, which ones are unavoidable, which ones are penalty fees that shouldn't be there, and how to find them on your own statement.

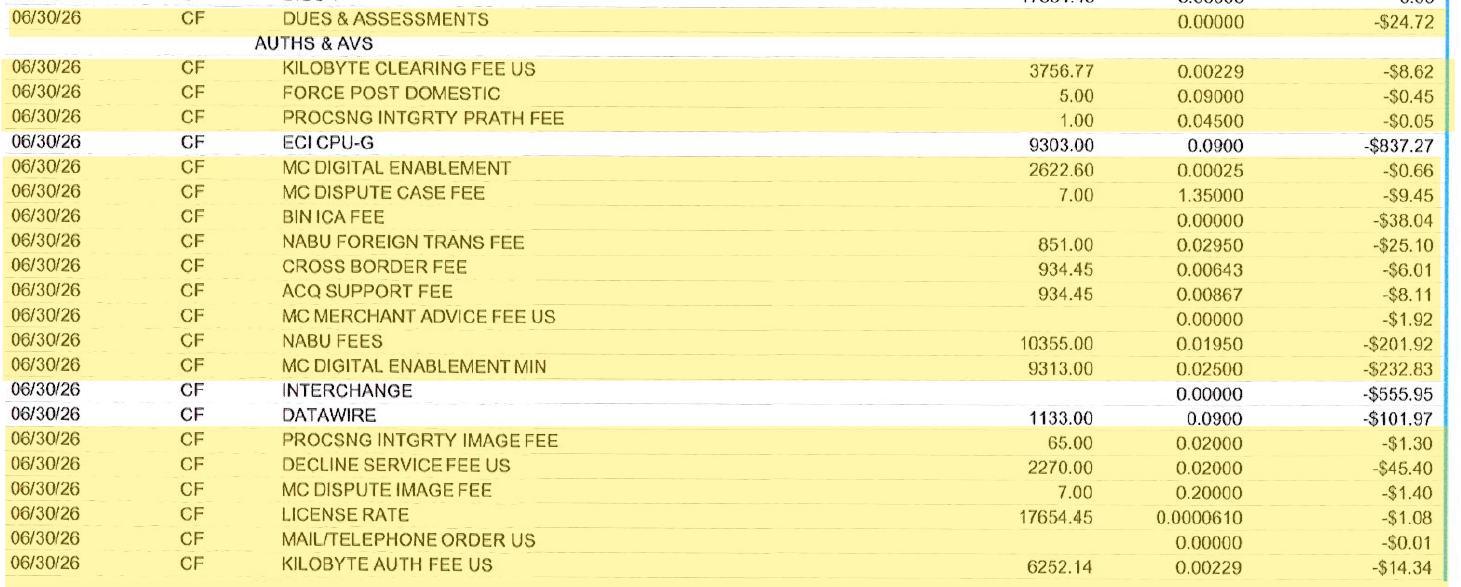

Actual snip of Mastercard Card Brand Fees. Come back when you’re done reading to see how many penalty fees you can find.

What Are Card Brand Fees?

Card brand fees are charges assessed by the payment networks themselves — Visa, Mastercard, Discover, and American Express — not by your payment processor.

This is an important distinction. Your processor's fees compensate them for their services. Card brand fees, on the other hand, go directly to the card networks. Your processor simply passes them through to you — they don't profit from them.

Card brand fees fall into two main categories:

· Unavoidable fees — standard charges that every merchant pays as a normal cost of accepting cards

· Penalty fees — charges triggered by specific processing issues that can often be fixed or eliminated

Unavoidable Card Brand Fees

Visa Fees

Visa Acquirer Processing Fee (APF)

Charged on every single Visa transaction processed. This is a small per-transaction fee that your processor passes through directly from Visa.

Visa Fixed Acquirer Network Fee (FANF)

A monthly fee that varies based on your business type and your total Visa processing volume. Every merchant that accepts Visa pays this — regardless of which processor they use.

Visa Assessment Fee

A percentage-based fee charged on your total monthly Visa sales volume. Currently 0.14% for credit card transactions and 0.13% for debit transactions.

Mastercard Fees

Mastercard Acquirer Program Support Fee (APSF)

A monthly fee based on your total Mastercard processing volume. Standard across all processors.

Mastercard Assessment Fee

A percentage-based fee on your total monthly Mastercard credit card volume. Currently 0.1375%.

Mastercard Network Access and Brand Usage Fee (NABU)

A small per-transaction fee charged on every Mastercard transaction. Currently $0.0195 per transaction.

Discover Fees

Discover Assessment Fee

A percentage-based fee on your total monthly Discover credit card volume. Currently 0.13%.

Discover Data Transmission Fee

A small per-transaction fee on every Discover transaction. Standard and unavoidable for all merchants accepting Discover.

American Express Fees

Amex Assessment Fee

Charged on all American Express transactions processed through the OptBlue program. This is a percentage-based fee on your monthly Amex volume.

A note on Amex OptBlue vs. Direct:

Merchants processing less than $3 million per year in American Express volume are typically set up under the OptBlue program, which means their Amex transactions are processed through their existing payment processor. Merchants processing over $3 million annually may have a direct relationship with American Express, which comes with a different fee structure.

International & Cross-Border Fees

When a customer pays with a card that was issued outside the United States, the card networks charge additional fees. These are known as international or cross-border fees, and they're easy to overlook.

Visa International Service Assessment (ISA)

Charged when a Visa card issued outside the U.S. is used at your business. Currently 0.40% on credit card transactions and 0.80% on debit and prepaid transactions.

Mastercard Cross-Border Fee

Charged when the card used is issued in a different country than where the merchant is located. Currently 0.60% for most transaction types.

How to find international fees on your statement:

Look for any of the following terms in your fee line items:

· "International Service Assessment"

· "Cross-Border Fee"

· "ISA Fee"

· "Intl" appearing next to a fee

These fees may be grouped with other card brand fees or listed separately depending on your processor's statement format.

If you rarely accept international cards, these fees should be minimal. If you see them frequently but don't serve international customers, it's worth taking a closer look — some processors mislabel or misapply these charges.

Penalty Fees — The Ones That Shouldn't Be There

Unlike the unavoidable fees above, penalty fees are triggered by specific issues in how transactions are processed. They are not a standard cost of doing business — and in many cases, they can be eliminated once the underlying cause is identified and corrected.

Visa Penalty Fees

Visa Transaction Integrity Fee (TIF)

Charged when a debit card transaction isn't processed in accordance with Visa's standards. This is most commonly caused by how the merchant's terminal is configured. Since it's a setup issue, it's generally fixable.

Visa Misuse of Authorization Fee

Charged when transaction authorizations aren't properly completed or reversed. This is typically a systems or process issue that can be corrected.

Visa Zero Floor Limit Fee

Charged when a transaction is settled without a proper prior authorization. Usually the result of a terminal or processing flow issue — and fixable once identified.

NVR APPRV REATTMPT (Never Approved Re-Attempt Fee)

This fee is charged when a merchant retries a transaction that was previously declined — without first obtaining a new, valid authorization. Card brand rules prohibit re-attempting a declined transaction without going through the proper authorization process again. This is a fixable issue, but one that requires awareness of the rules around declined transactions.

Mastercard Penalty Fees

Mastercard Electronic Commerce Merchant (ECM) Fee

Charged on e-commerce transactions that aren't properly authenticated. This is often resolved by updating gateway settings to ensure correct authentication protocols are in place.

Mastercard Processing Integrity Fee

Similar in nature to Visa's Transaction Integrity Fee — charged when transactions aren't processed according to Mastercard's standards. Usually a setup or configuration issue.

Mastercard Account Status Inquiry Fee

Charged when excessive authorization checks are made without a corresponding completed transaction. A systems or process adjustment typically resolves this.

What Triggers Penalty Fees?

Penalty fees don't appear randomly. They're the result of specific, identifiable issues — most of which are preventable. Common triggers include:

Terminal setup issues

An incorrectly configured terminal is one of the most frequent causes of penalty fees. Most merchants aren't aware their terminal isn't set up properly until the fees start showing up on their statement.

Incorrect transaction flow

The way a transaction moves through the authorization, capture, and settlement process matters. Any deviation from card brand rules can trigger fees.

Re-attempting declined transactions

Every time a merchant retries a transaction that was declined — without a new authorization — the NVR APPRV REATTMPT fee is assessed. This is a rule many merchants simply aren't aware of.

Outdated equipment or software

Older terminals may no longer meet current card brand processing standards, resulting in recurring penalty fees that continue month after month.

E-commerce authentication gaps

Online transactions that aren't properly authenticated using 3D Secure or other required protocols can trigger the Mastercard ECM fee and similar charges.

How to Find Card Brand Fees on Your Statement

Knowing what these fees are is only half the battle — you also need to know where to look for them.

Step 1: Find the card brand or network fees section

Most processors group these fees together under a section labeled "Card Brand Fees," "Network Fees," or "Association Fees." Some processors, however, scatter them throughout the statement as individual line items.

Step 2: Match the fee names

Cross-reference what you see on your statement with the fee names covered in this guide. Each card brand — Visa, Mastercard, Discover, Amex — has its own set of fees with specific names.

Step 3: Separate unavoidable fees from penalty fees

Assessment fees, NABU, APF, FANF, and ISA fees are normal and expected. Transaction Integrity Fees, Processing Integrity Fees, Misuse of Authorization Fees, and NVR APPRV REATTMPT fees are red flags.

Step 4: Pay attention to the totals

Individual card brand fees can seem small on their own, but they accumulate quickly at volume. A $0.10 fee charged on 5,000 monthly transactions adds up to $500 per month — $6,000 per year.

The Bottom Line

Card brand fees are a permanent part of accepting credit and debit cards. The unavoidable ones — assessments, per-transaction fees, network fees — are the same regardless of which processor you use, and they belong on your statement.

The penalty fees, however, are a different story. If you're seeing Transaction Integrity Fees, Processing Integrity Fees, Misuse of Authorization Fees, or NVR APPRV REATTMPT fees on your statement — something in your processing setup needs attention. These fees can often be eliminated once the root cause is identified.

Understanding the difference between the two is the first step to taking control of your processing costs.

Have Questions About Your Statement?

At Save Solutions, we help merchants make sense of their processing statements — identifying what's normal, what shouldn't be there, and what can be done about it.

If you'd like a second set of eyes on your statement, we're happy to help.

📞 (347) 528-3723

📧 info@savesolutionsnj.com

🌐 www.savesolutionsnj.com